INCOME TAX

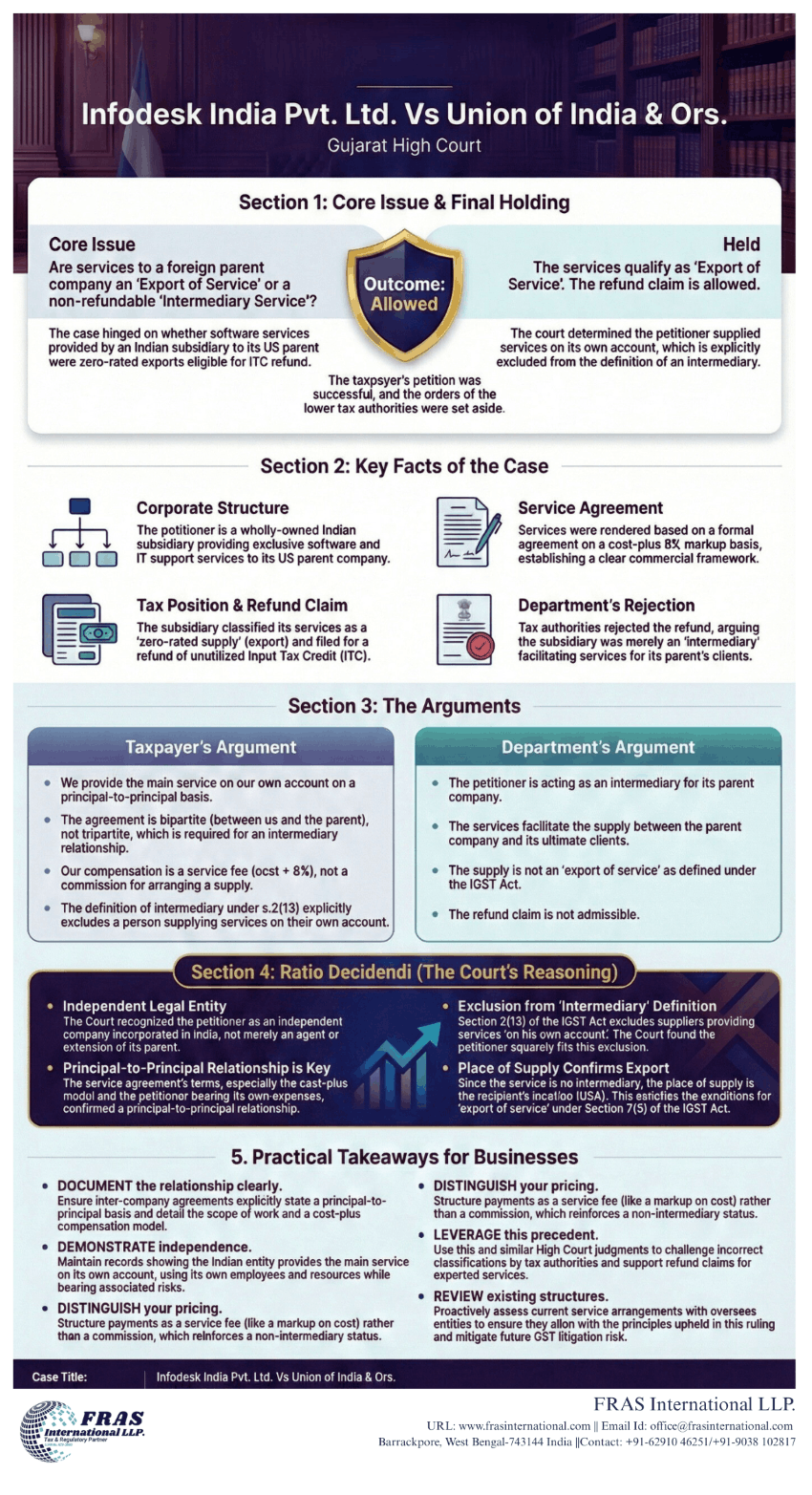

Taxpayer's Argument

- We provide the main service on our own account on a principal-to-principal basis.

- The agreement is bipartite (between us and the parent), not tripartite, which is required for an intermediary relationship.

- Our compensation is a service fee (ocst8%), not a commission for arranging a supply.

- The definition of intermediary under s.2(13) explicitly excludes a person supplying services on their own account.

Department's Argument

- The petitioner is acting as an intermediary for its parent company.

- The services facilitate the supply between the parent company and its ultimate clients.

- The supply is not an 'export of service' as defined under the IGST Act.

- The refund claim is not admissible