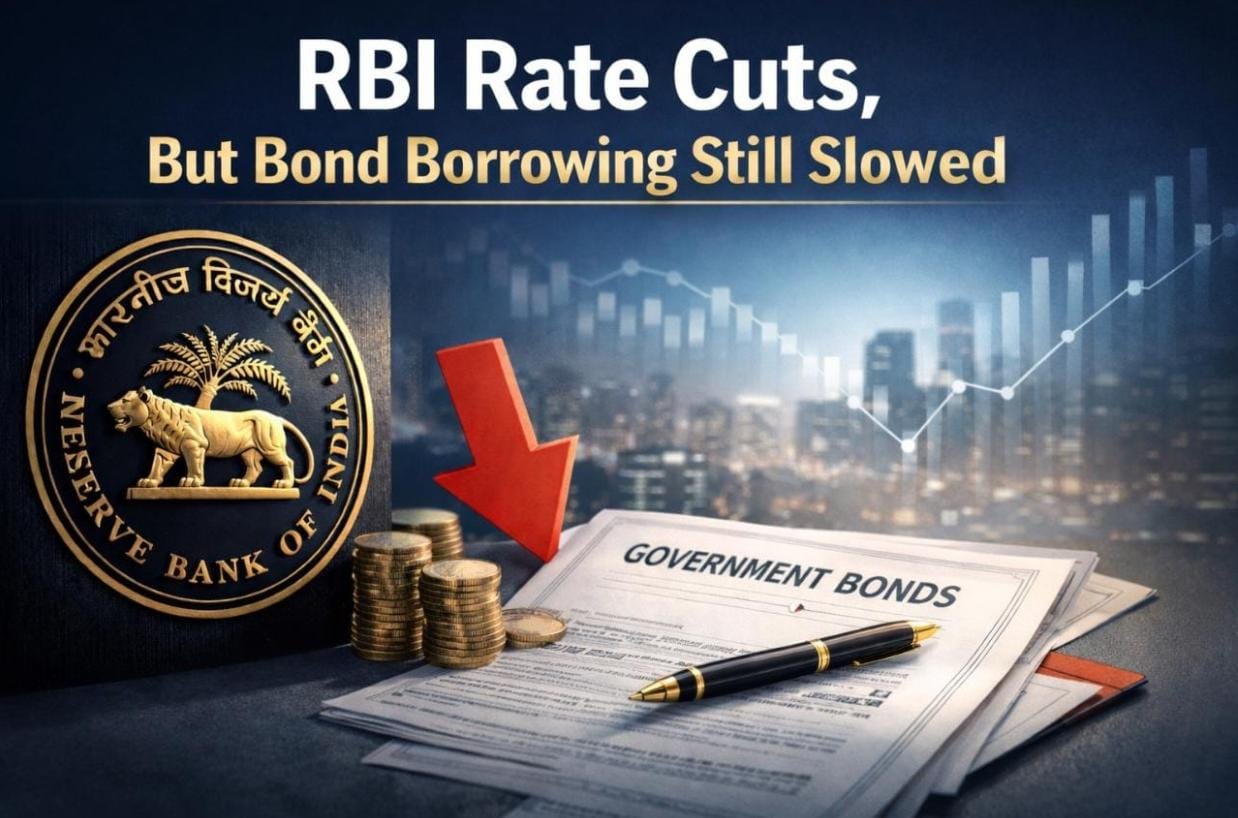

Why are Indian companies raising LESS money through corporate bonds this year?

First: What is a corporate bond?

When a company needs funds, it can either:

Take a loan from a bank, or

*Borrow directly from investors by issuing bonds

A corporate bond simply means:

> The company borrows money from investors, pays interest, and repays the amount later.

What did RBI do this year?

To support borrowing, RBI:

* Cut interest rates by 1.25%

* Injected additional liquidity into the banking system

* Relaxed certain lending norms for banks

In theory, this should have made bond borrowing cheaper.

But that did not fully happen.

What actually happened?

* Corporate bond borrowing fell by around 6% compared to last year

* More companies accessed the bond market

* But they raised smaller amounts overall

Why borrowing looked strong early in the year

April–June period:

* Companies expected interest rates to fall further

* Bond yields were already softening

So many companies decided to borrow early, saying:

> “Let’s raise funds now before conditions change.”

Result:

* Very strong bond issuance in the first quarter

* Weak bond activity in later months

Global shocks changed the situation

After June, global uncertainty increased:

US imposed 50% tariffs on Indian goods

* Rupee weakened

* Foreign investors turned cautious

When global risk rises, market interest rates tend to move up.

Heavy government borrowing pushed yields higher

At the same time:

* Central government issued large volumes of bonds

* State governments also increased borrowing

Simple rule:

More bonds in the market = higher interest rates

So:

* Government bond yields rose

* Corporate bond yields also moved up

If RBI cut rates, why did bond interest rise?

This is the key point:

* RBI controls short-term interest rates

* Long-term rates are decided by the market

Markets reacted to:

* Heavy government borrowing

* Global uncertainty

* Weak rupee

Result:

* Long-term bond yields remained high

* Corporate bonds did not become cheap

Bank loans became cheaper than bonds

* Bank lending rates came down

* Corporate bond yields stayed elevated

So companies compared:

Bank loans = cheaper

Bonds = expensive

Decision was straightforward:

> Why issue bonds when bank loans are cheaper?

Many companies:

* Cancelled bond issuances

* Shifted borrowing to banks

Even banks issued fewer bonds

Banks themselves:

* Had sufficient deposits

* Received liquidity support from RBI

* Did not need to raise funds via bonds

Since banks are major bond issuers, their reduced participation further slowed the bond market.

Long-term borrowing became costly

Companies looking to borrow for:

* 10 years

* 15 years

* 20 years

Found that:

* Long-term bond yields were too high

* Cost of borrowing was unattractive

As a result, long-term bond issuance declined sharply.

Companies used alternative funding sources

Instead of bonds, companies preferred:

* Bank loans

* Foreign borrowings

* Syndicated loans

These options were:

* More flexible

* Sometimes cheaper

* Easier to manage

What could happen next Experts expect:

* Continued RBI liquidity support

* Stronger bank lending capacity

* Possible slowdown in government borrowing

This may gradually ease bond yields and revive corporate bond issuance.

Bottom Line

Despite RBI rate cuts, global uncertainty, heavy government borrowing and cheaper bank loans kept corporate bond yields high. As a result, companies reduced bond borrowing and shifted towards bank loans and alternative funding sources.

Read More